Michael P. Phipps, Managing Director, New Republic Partners

When it comes to hedge funds, too many investors and their advisors have been thinking about them too simplistically for far too long. By that I meant that hedge funds are by and large viewed as a monolithic asset class in portfolio implementation.

One size and strategy fits all, if you will. We believe that’s a misguided approach. We assert that hedge funds should be considered more of a “construct” that offers investors an incredible variety of strategies across a range of portfolio roles like diversification, growth, and income. To lump hedge funds together as “one thing” within a portfolio is to do them — and the impact they can have on investors’ expectations — a grave disservice.

If you have been led to believe hedge fund-of-funds provide a greater level of diversification, you may also want to rethink that assumption. Most fund-of-funds aggregate all hedge funds together without allowing for a thoughtful approach to allocation and consideration as to why they are in a portfolio in the first place. Again,they are essentially treated as a singular purpose within a portfolio. We believe that approach presents a significant lost opportunity.

As the headline of this article asserts, not all hedge funds are created equal … not by a long shot. Granted, many investors don’t care considering U.S. equity has compounded at 13% over the past seven years.1 However, as the common footnote disclosure goes, past performance is not indicative of future returns, and we would argue that the environment for hedge fund investing has markedly improved in the past two years. Advisors and the investors they work for would be wise to begin treating hedge funds as the nuanced, highly specialized players they are within a sophisticated investment portfolio.

Rethink diversification

As mentioned above, too many financial advisors and investors view hedge funds through the simplistic lens of just adding diversification. Of course, diversification is not a bad thing. It’s essential to most investors’ portfolios and has been called the only “free lunch” in finance. In many cases, hedge fund strategies do act as diversifiers and are additive to a portfolio. Their low correlations with the traditional assets of equities and fixed income can decrease portfolio volatility and risk while still driving attractive returns. However, adding diversification requires understanding to what degree a hedge fund investment correlates (or does not correlate) with the public equity and fixed income portions of an investment portfolio. Without diving into great detail, the chart below highlights the wide spread of correlations between select hedge fund strategies and traditional assets (from low-to-no correlation in blue to highly correlated in dark red).

Consider hedged equity

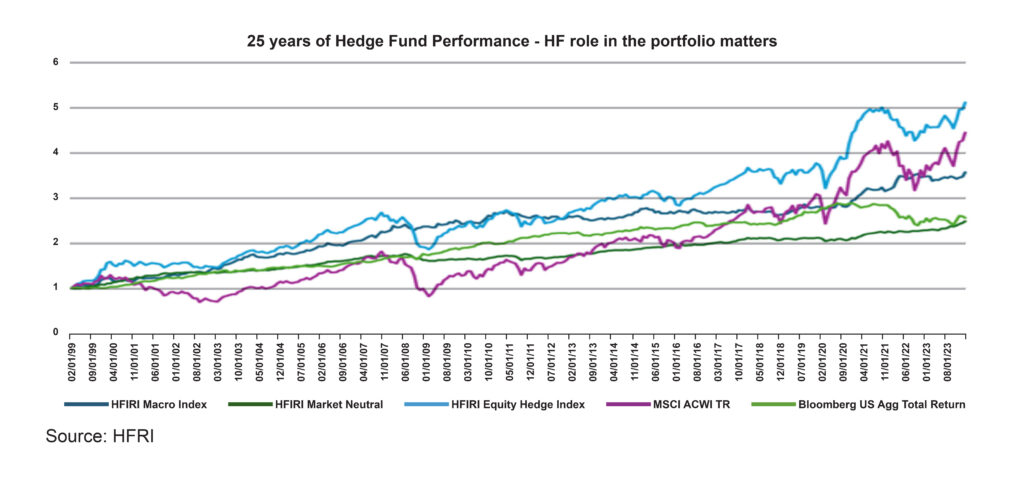

As stated, diversification is a primary feature of hedge funds, but it is not always the primary reason to invest in them. There are many strategies that are return-seeking more than they are risk-reducing. Consider the “traditional” long/short equity manager or “hedged equity.” While hedged equity investing provides less of a diversification benefit (note the higher “red” correlation of the broad HF index and hedged equity with the equity indices above), it can be additive to a portfolio given its higher return expectations compared to other hedge fund strategies that have more of a fixed income-like profile. That is because hedged equity involves a degree of underlying public market exposure. The chart below highlights the historical returns of select hedge fund strategies where one can see how certain strategies are more equity-like (e.g. hedged equity), some are more bond-like (market neutral) and some “dance to their own tune” (macro).

Hedged equity combines a modest degree of public market exposure (beta), with the fund manager’s skill in picking stocks either long or short (alpha). In the right portfolio construct, that alpha+beta combination has the potential to outperform long-only equities over the long run (as the chart also highlights). However, because hedged equity involves finding alpha, it requires additional due diligence to gain confidence that the hedge fund portfolio managers in consideration can sustainably generate returns in excess of the market, net of fees.

Know your “why” behind investing in hedge funds

As the premise of this article states, there are a wide variety of strategies that can be employed through investing in hedge funds. In order to harness that flexibility, it is important to be clear about the specific reasons for having hedge funds in a portfolio. What role do they play? Is it for diversification, growth, or income? What is the benchmark you are seeking to beat (net of fees)? Is it equities, fixed income, or an absolute return hurdle? Again, investing in hedge funds allows for significantly more latitude in how assets are invested. Hedge fund managers can invest long or short in equities and across asset classes in foreign exchange (fx), interest rates, credit, derivatives, and even crypto currency if they so desire. In other words, hedge funds open up the gates of investing options, versus a traditional mutual fund. However, that puts the onus on investors and their advisors to perform due diligence and select and prudently place hedge funds within a portfolio with the proper bounds and expectations.

Broadly speaking, we believe the wealth management industry misses this distinction and continues to treat hedge funds as a monolithic “diversifying” asset class. The bottom line is this: if you don’t know why you are investing in hedge funds, you are likely to have a mediocre result. If diversification is the goal, you may be comfortable with bond-like returns from an asset that acts like a ballast to your portfolio or has a major payoff when markets crash. Alternatively, if you are investing in hedge funds to hopefully realize out- sized returns, then you should be comfortable with more downside risk. As in life, setting expectations is a key exercise. The point being: not understanding your “why” when investing in hedge funds will likely result in disappointment.

1S&P 500® Index through December 31, 2023

Michael P. Phipps is a managing director at New Republic Partners and serves on the firm’s executive committee and investment committee. He is actively involved in all aspects of portfolio management for the firm’s clients, including asset allocation, portfolio construction and investment diligence. Phipps has extensive experience in asset management and endowment management for high-net-worth and large institutional clients.

Reach him at info@newrepublicpartners.com

About New Republic Partners

New Republic Partners is an innovative investment management and wealth advisory firm serving affluent families, RIAs, endowments and foundations. We believe that clients benefit from access to investment opportunities usually reserved for large institutional investors and the expertise and experience of a successful and seasoned investment management, wealth advisory and family office solutions team. The firm is headquartered in Charlotte, North Carolina, and serves clients across the U.S. with regional offices. More information can be found at New Republic Partners.

New Republic Partners is an investment advisor registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about New Republic Partners’ advisory services can be found in its Form ADV Part 2 and/or Form CRS, which are available upon request. Material presented has been derived from sources considered to be reliable, but accuracy and completeness cannot be guaranteed.

The opinions expressed are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Forward-looking statements cannot be guaranteed.

The S&P 500® Index is the Standard & Poor’s Composite Index and is widely regarded as a single gauge of large cap U.S. equities. It is market cap weighted and includes 500 leading companies, capturing approximately 80% coverage of available market capitalization.

The MSCI ACWI NR Index is a global equity index that captures large and mid-cap representation across 23 developed markets and 27 emerging markets. The index covers approximately 85% of the global investable equity opportunity set.

The Bloomberg Barclays U.S. Aggregate Bond Index is a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States. The Index is frequently used as a stand-in for measuring the performance of the U.S. bond market. In addition to investment grade corporate debt, the Index tracks government debt, mortgage-backed securities (MBS) and asset-backed securities (ABS) to simulate the universe of investable bonds that meet certain criteria. In order to be included in the Index, bonds must be of investment grade or higher, have an outstanding par value of at least $100 million and have at least one year until maturity.

The volatility (beta) of an account may be greater or less than its respective benchmark. It is not possible to invest directly in an index. Past performance is not indicative of future results.